Life insurance isn’t just a financial product — it’s peace of mind. It’s a safety net for your family, a tax strategy tool, and in some cases, a long-term wealth-building asset. Still, one of the most common questions people ask is:

“Should I choose term life or whole life insurance?”

There’s no one-size-fits-all answer. The right policy depends on your current situation, future goals, and how you want to protect or pass on your wealth.

Here’s what you need to know to make an informed choice.

Understanding the Basics: Term vs. Whole Life Insurance

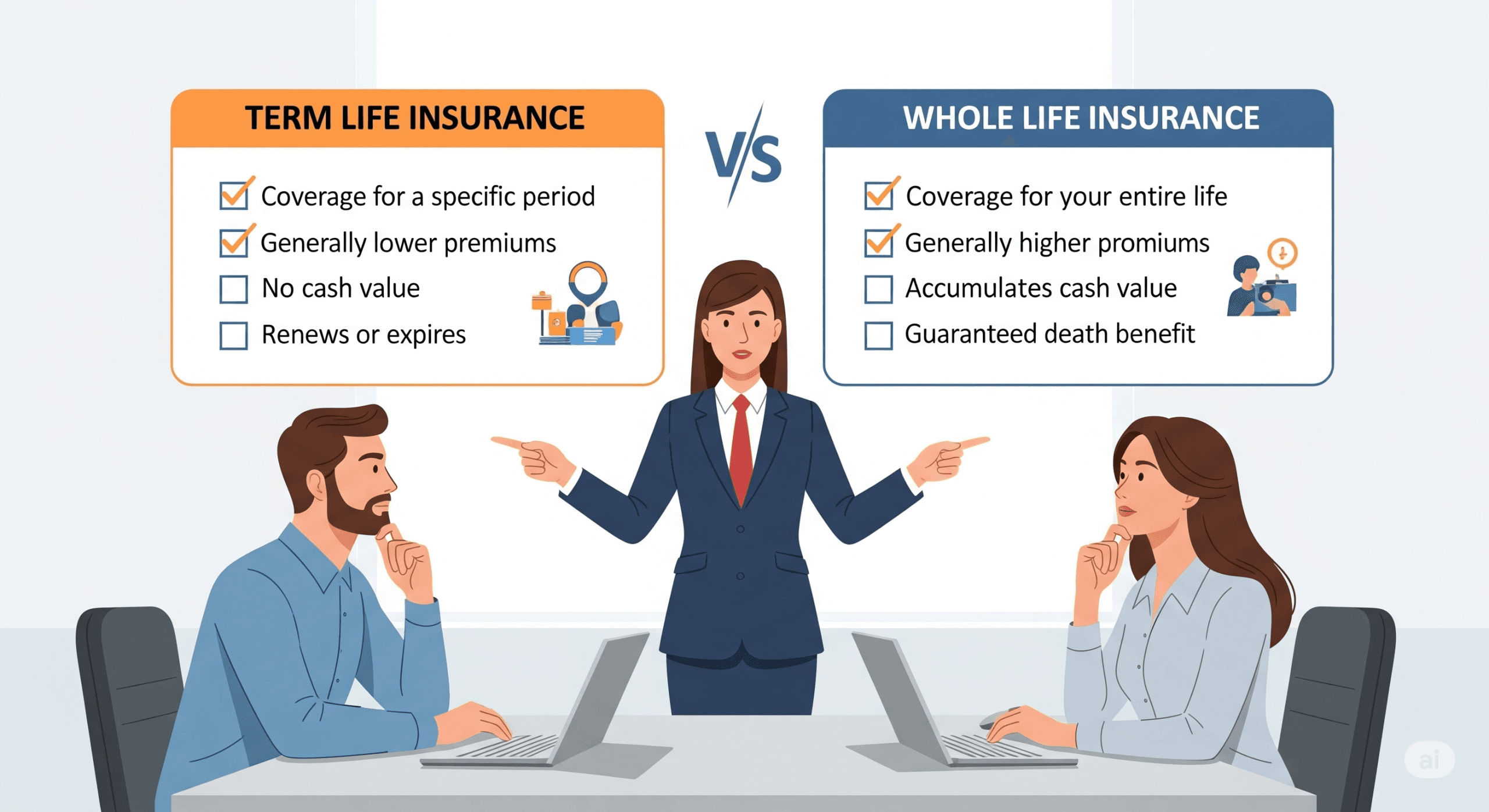

Term Life Insurance

Covers a specific time frame (10, 20, or 30 years)

Only pays out if the policyholder dies within that term

Lower premiums compared to whole life

Offers no cash value — strictly for protection

Term life is straightforward, affordable, and works well for temporary needs like mortgage protection or income replacement while raising a family.

Whole Life Insurance

Covers you for your entire life (as long as premiums are paid)

Builds cash value over time

Offers tax-deferred growth

Premiums are higher, but benefits go beyond just coverage

Whole life blends protection with savings and legacy planning — appealing to those looking to create financial security across generations.

When Term Life Insurance Makes Sense

Term life may be the better option if:

You’re under 50 and want affordable protection

You have dependents, a mortgage, or other financial obligations

You’re a new parent or small business owner looking to protect income

You need coverage for a fixed period (e.g., until your kids are grown)

Real-World Example:

A 34-year-old entrepreneur wanted insurance coverage while building his business. A 20-year term policy gave his family financial protection without straining his monthly budget, allowing him to invest more into his company.

When Whole Life Insurance Is the Better Fit

Whole life is often a smarter move if:

You want permanent coverage that lasts a lifetime

You’re focused on wealth transfer or estate planning

You have long-term goals for building cash value

You want guaranteed returns with tax advantages

Scenario Spotlight:

A couple preparing for retirement wanted to pass on wealth to their grandchildren. A tailored whole life insurance policy gave them lifetime coverage and a tax-efficient legacy strategy — all in one solution.

Not Sure Which Is Right for You? Here’s a Quick Comparison:

| Feature | Term Life | Whole Life |

|---|---|---|

| Coverage Length | 10–30 years | Lifetime |

| Premium Cost | Lower | Higher |

| Cash Value | No | Yes (builds over time) |

| Investment Element | None | Yes, fixed returns |

| Best For | Young families, startups | High earners, estate planners |

| Purpose | Income protection | Legacy + long-term financial growth |

Life Insurance Is More Than Just Numbers

Choosing a policy isn’t only about premiums and death benefits. It’s about aligning your insurance with your broader life and financial goals.

Consider questions like:

Do you plan to retire early or later?

Will you have dependents or beneficiaries with long-term needs?

Are you concerned about estate taxes?

Are you building wealth to pass on?

Do you own a business that would need succession planning?

These answers shape what type of insurance — and how much — you truly need.

The Real Strategy Behind a Smart Policy

Many online calculators give you a number based on income and age, but that’s just a starting point. The best policies are those that factor in the bigger picture: your business, your legacy, your family, your taxes.

Insurance isn’t a checkbox — it’s part of your overall financial architecture. And it should evolve as your life does.

Whether you’re just starting or preparing for retirement, the right life insurance policy can be one of the most important decisions you make for your future and your family.

Want personalized advice beyond what online tools can offer?

That’s where experienced financial consultants come in. For example, Irina Tamarova, known for her work with entrepreneurs and families alike, has helped many navigate these choices not as a sales agent, but as a strategist. Her work — through Macrotech — bridges financial protection with legacy planning, ensuring that insurance fits your life, not just the brochure.

If you’re serious about protecting your loved ones and building a smart financial future, a conversation with a seasoned expert may be the smartest next step.