Navigating Medicare can feel overwhelming — especially when you’re managing a business, supporting family, or preparing for retirement. Between deadlines, plan options, penalties, and changing rules, even well-informed individuals can get tripped up.

But understanding Medicare isn’t just about checking a box — it’s about making smart choices that impact your healthcare, retirement income, and long-term financial security.

Here’s a simple, up-to-date breakdown of what you need to know about Medicare in 2025.

Why Medicare Matters More Than Ever

Healthcare costs are one of the largest — and most underestimated — threats to retirement savings. For many, Medicare is the core of their health coverage once they leave an employer plan or turn 65. But Medicare decisions aren’t just about picking the lowest premium. They affect:

Your access to doctors and medications

Your ability to cover unexpected expenses

Your long-term care and estate planning

Your retirement tax strategy

Whether you’re enrolling for yourself or helping a loved one, getting Medicare right is essential.

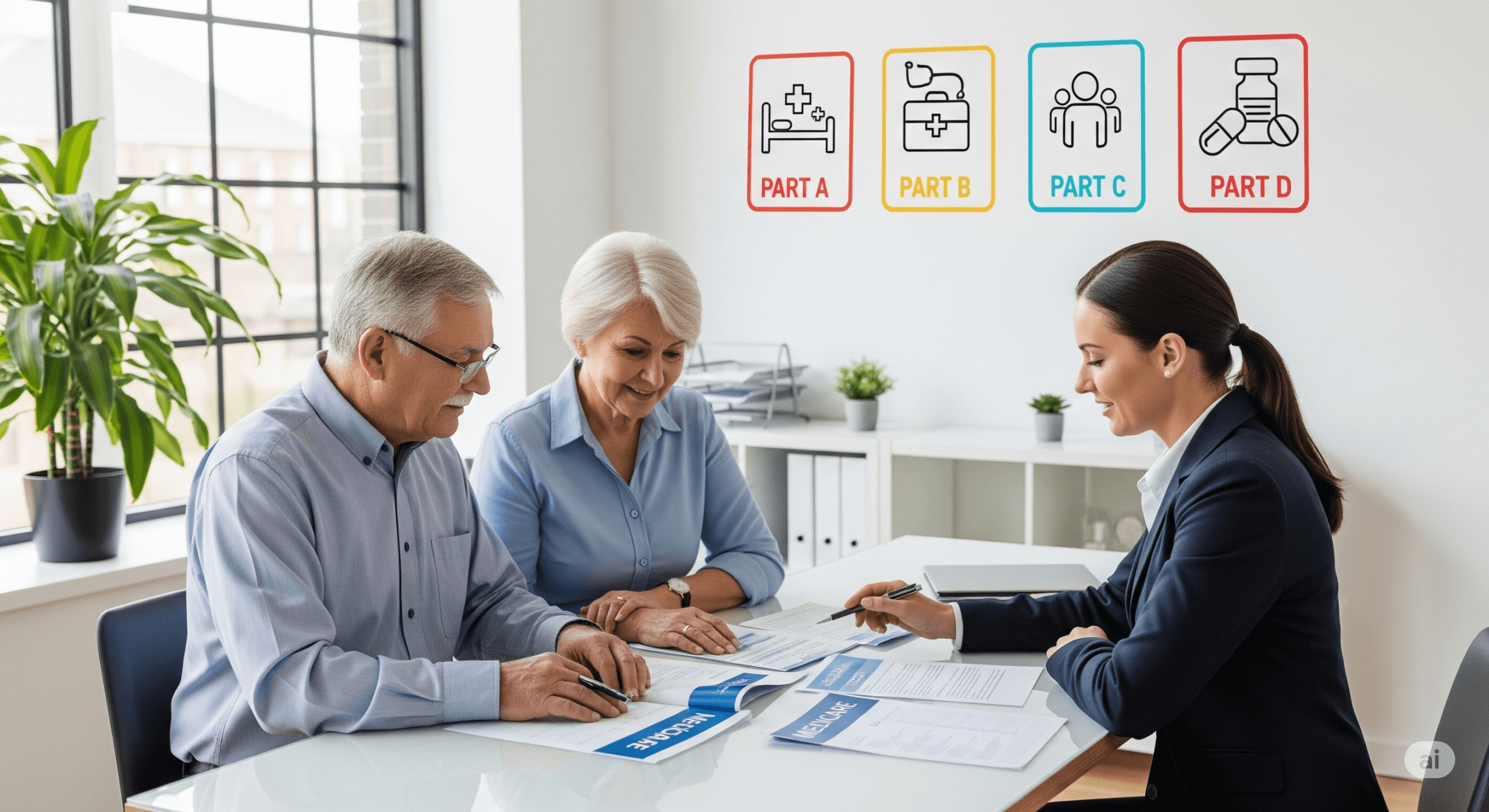

What Does Medicare Include?

Medicare is a federal health insurance program available to:

People age 65 or older

Younger individuals with certain disabilities

Those with End-Stage Renal Disease

The program has four major parts:

Part A: Hospital insurance

Part B: Doctor visits, outpatient services

Part C (Medicare Advantage): A private plan that combines A & B (and sometimes D)

Part D: Prescription drug coverage

You can stick with “Original Medicare” (Parts A and B) or opt for an Advantage plan (Part C). Each has trade-offs in coverage, cost, and provider access.

When to Enroll in Medicare

Timing your enrollment is critical. Miss your window, and you could face lifelong penalties.

Key Enrollment Periods:

Initial Enrollment Period (IEP): Starts 3 months before your 65th birthday and ends 3 months after.

General Enrollment Period (GEP): January 1 – March 31 if you missed your IEP. Coverage starts in July.

Special Enrollment Period (SEP): If you’re losing employer coverage or moving states, you may qualify.

Common Medicare Mistakes to Avoid

Missing enrollment deadlines

Delaying Part B without employer coverage

Skipping Part D and facing penalties later

Assuming Medicare pays for everything (it doesn’t)

Choosing a plan based on premium alone instead of total costs

What to Consider Before Picking a Plan

When evaluating Medicare options, look beyond just monthly costs. Ask yourself:

Are my doctors in-network?

What’s the annual out-of-pocket limit?

Will my medications be covered?

Do I travel frequently or live in multiple states?

Do I need dental, vision, or hearing coverage?

For those still working or running a business at age 65, the decisions get more complex. It’s essential to coordinate Medicare enrollment with employer-provided insurance, HSAs, and retirement distributions.

Real Example: A Smart Medicare Strategy for a Business Couple

A couple in Texas — both nearing retirement and running a logistics company — had several questions:

Should we enroll in Part B now or later?

Is Medicare Advantage better for our budget?

How does Medicare fit with our retirement withdrawals?

A carefully mapped plan helped them:

✔ Coordinate employer and Medicare coverage

✔ Model total annual costs for different plan types

✔ Stagger enrollment to avoid penalties

✔ Align healthcare planning with retirement income strategy

By thinking ahead, they saved over $6,000 annually — and avoided rushed decisions.

Medicare decisions can’t be made in a vacuum. They’re part of a broader conversation about health, family, and financial independence.

If you’re:

Turning 65 soon

Still working and unsure when to enroll

Helping aging parents manage their healthcare

Trying to align your Medicare choices with retirement or tax planning

— it may be time to speak with someone who sees the full picture.

One such expert is Irina Tamarova, a business and retirement consultant who helps individuals and families make Medicare decisions with clarity and long-term confidence. Through her firm, Macrotech, she’s worked with entrepreneurs, professionals, and retirees to connect the dots between health insurance, taxes, and legacy planning — with zero jargon or pressure.